Strong Rebound of US B2B Exhibition Industry Continues

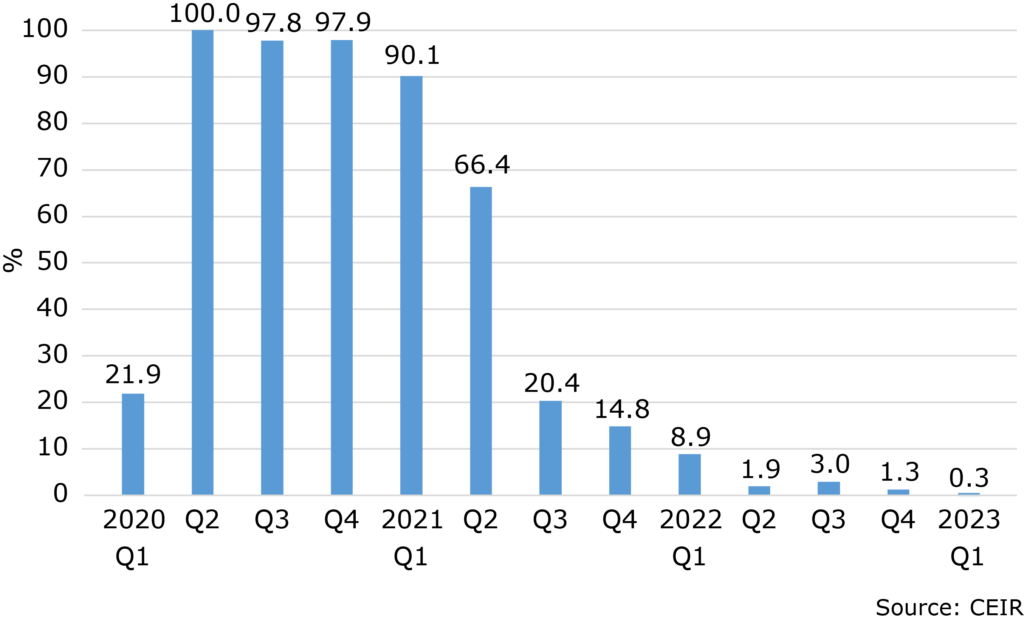

DALLAS, 20 July 2023 – The Center for Exhibition Industry Research (CEIR) announced today that the U.S. business-to-business (B2B) exhibition industry continues to rebound, recording a continued improvement in Q1 2023 from the previous 12 quarters. The cancellation rate for physical in-person events dropped to 0.3%, which is a dramatic improvement from 90.1% in Q1 2021 and 8.9% in Q1 2022.

Figure 1: B2B Exhibition Industry Cancellation Rate, %

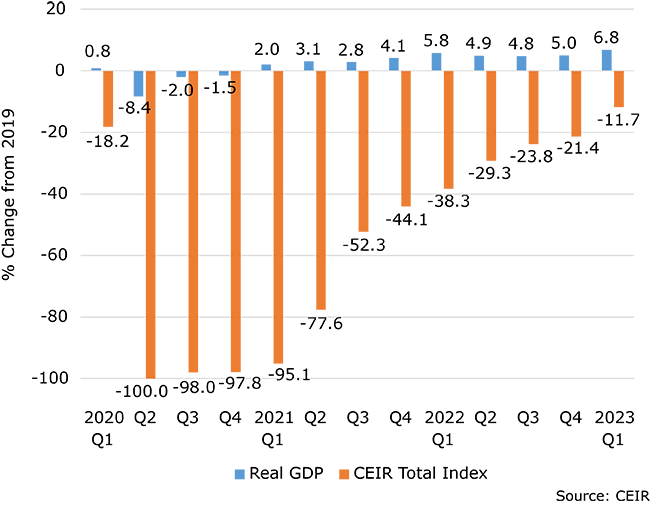

Extremely low cancellations and continued improvement in metrics outcomes for completed events boosted the Q1 2023 Index result. As expected, the CEIR Total Index – a measure of overall exhibition performance – continues to recover, surging 42.7% from a year ago. Compared to Q1 2019, it was still 12.0% lower as shown in Figure 2 below. Nonetheless, this is a vast improvement compared to the past two years, which included declines of 95.1% from 2019 in Q1 2021 and 38.3% from 2019 in Q1 2022.

US GDP and the CEIR Total Index

The performance of the U.S. economy was far better, registering a 6.8% increase in real (inflation-adjusted) GDP from Q1 2019 to Q1 2023. On a seasonally-adjusted annual rate (SAAR) basis, after two consecutive quarters of increase in Q3 2022 (3.2%) and Q4 2022 (2.6%), real GDP rose at a modest rate, gaining 2.0% in Q1 2023. The continued rebound in Q1 primarily reflected increases in consumer spending, exports, government spending at all levels and nonresidential fixed investment that were partly offset by decreases in private inventory investment, residential fixed investment and increases in imports.

Up to Q4 2021, economic recovery had been led by strong spending on goods. However, the initially sluggish recovery in services industries recently has continued to pick up the pace. In Q3 2021, real spending on consumer services finally recovered pandemic losses and robust expansion has continued since then. In Q1 2023, real spending on consumer services exceeded Q4 2019 spending levels by 4.8%.

Figure 2: Real GDP vs. CEIR Total Index, Q1 2020-Q1 2023, % Change from 2019

Q1 2023 Exhibition Industry Performance – Recovery Momentum Continues

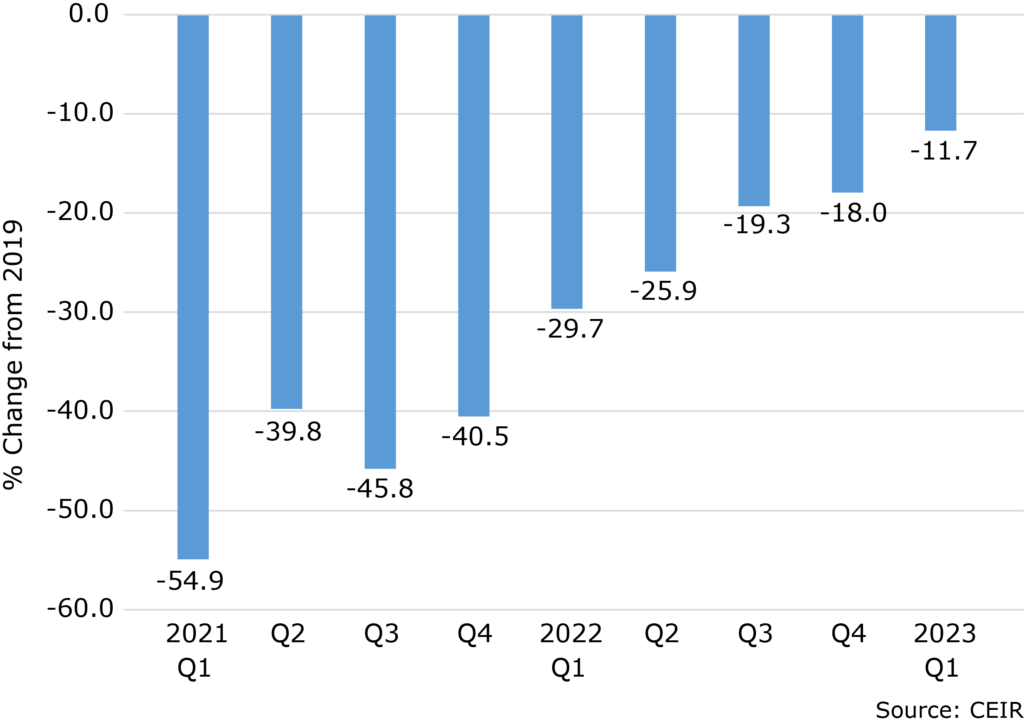

Figure 3 provides insights about events completed during Q1 2021 to Q1 2023, comparing performance of each to the same quarter in 2019. Q1 2023 results speak to a continuing recovery that is underway with the overall Index and specific metrics improving for the past eight quarters. Among completed events, 33.3% have surpassed their pre-pandemic levels of the CEIR Total Index. This is double the percentage of completed events that surpassed pre-pandemic levels in Q1 2022, where 15.3% of events held in that quarter surpassed 2019 results. Some organizers launched new shows, expanded existing shows to new locations or held them at a different time of the year. When looking at results excluding cancellations, performance of events that happened in Q1 2023 documents continued improvement; it is down only 11.7% compared to 2019 (Figure 3), which is much better than the decline of 29.7% registered in Q1 2022 compared to 2019.

Figure 3: CEIR Total Index Excluding Cancellations, % Change from 2019

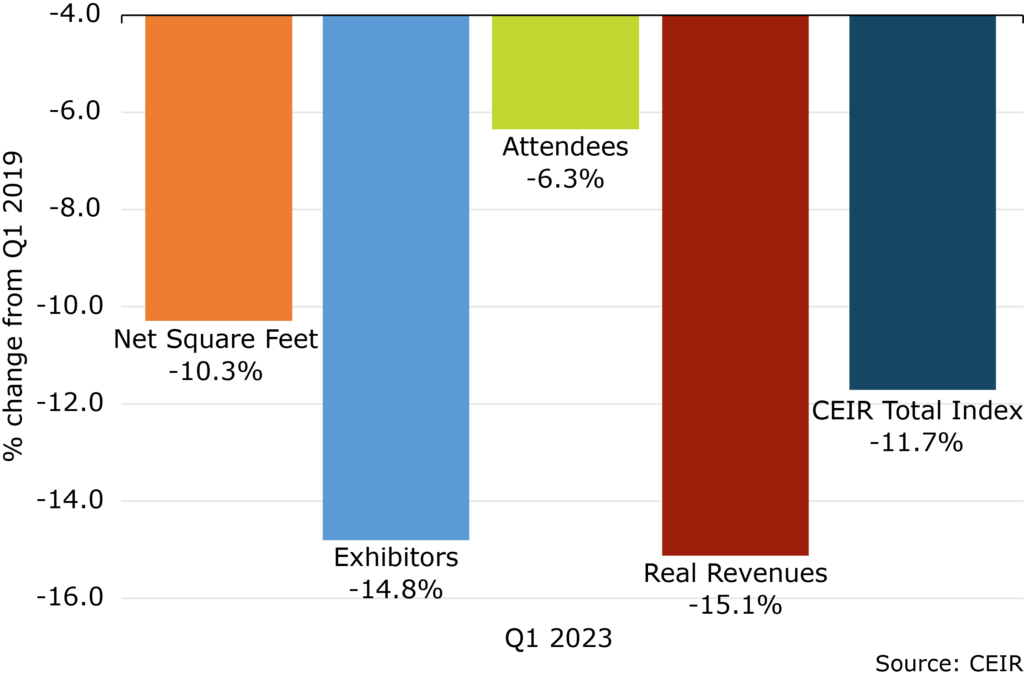

Among the four metrics, Attendees has recovered the most, just 6.3% below results registered in Q1 2019; followed by Net Square Feet (NSF) with a decline of 10.3%. Exhibitors is 14.8% below Q1 2019. Real Revenues in Q1 was the metric that contracted the most at 15.1% from Q1 2019, as nominal revenue levels remained low and high inflation further eroded the value of this income.

Figure 4: Q1 2023 CEIR Metrics for the Overall Exhibition Industry Excluding Cancellations, % Change from Q1 2019

Insights on a Recession

The turmoil among U.S. regional banks is not having as much of an impact on economic activities as analysts feared in March. Recent economic indicators such as consumer spending, payroll employment and job openings to unemployed ratio indicate that the economy has been resilient. The long-awaited recession is still nowhere in sight. Nonetheless, the impact of monetary tightening on the economy tends to have a long lag. With two more interest rate hikes (25 basis points each) expected, economic growth could decelerate further during the second half of the year.

The probability of a recession starting in 2023 is now lower, standing at 50%. The potential causes of recession include tighter financial and credit conditions, a self-fulfilling prophecy, and some unknown and unpredictable shocks. Businesses that anticipate a recession ahead are cutting back their expenses and head counts. However, if there is recession, it likely will be shallow as household debt service payments as a percent of disposable income remain low even though they have inched up recently, there is pent-up consumer demand for services such as travel and tourism, most large corporations still are flush with cash, and there is a race to adopt new technologies such as AI (artificial intelligence) and EV (electric vehicles).

B2B Exhibitions Recovery

The second half of 2023 through the first half of 2024 will be challenging for the exhibition industry as the economy slows down further and businesses are more cautious. Nonetheless, “the positive momentum of participation in face-to-face trade shows will continue. Widespread B2B exhibition cancellation is a thing of the past except for permanent closure of shows, and the performance of completed events will continue to improve,” said CEIR Economist Dr. Allen Shaw, Chief Economist for Global Economic Consulting Associates, Inc. “Greater numbers of foreign participants will support additional recovery of volume of attendance and exhibitors. A full recovery for the industry is expected in 2024.” Among 14 industry sectors that CEIR monitors, the Government and Discretionary Consumer Goods and Services sectors are expected to perform better, whereas the Communications and Information Technology and Building, Construction, Home and Repair sectors will lag behind the overall exhibition industry.

“CEIR research has documented an intent to return to face-to-face engagement at B2B exhibitions, and CEIR Index quarterly results continue to document the recovery is in progress,” added CEIR CEO Cathy Breden, CMP-F, CAE, CEM. “Each quarter, the Index is showing that more business professionals and exhibitors are coming back to the B2B exhibitions channel to meet their marketing, sales and business information needs.”

CEIR has released the 2023 CEIR Index Report, which analyzes the 2022 exhibition industry performance and provides an economic and exhibition industry outlook for the next three years. CEIR collects data directly from B2B exhibition organizers, who are encouraged to provide their show data by using the Event Performance Analyzer. In exchange for submitting data for a valid B2B exhibition, the participants are provided this tool which enables an organizer to instantly see how an event’s performance compares to CEIR Index benchmarks at no cost. Data submission is strictly confidential. Click here for more information. The annual CEIR Index Report for their shows’ market sector will also be provided to participating organizers at no cost.

Explanation and Definitions of Q1 Comparisons

As explained above, 8.9% of trade shows scheduled to be held in the first quarter of 2022 were cancelled, limiting the usefulness of comparisons of Q1 2022 and Q1 2023 results, as any positive change would be very large and misleading. A more useful comparison is to the 2019 performance results, measured as the industry benchmark before COVID-19 forced the shutdown. Thus, events in the first quarter of 2023 are compared with those in the first quarter of 2019 in Figures 2-4. The CEIR Total Index in Figure 2 is a weighted average that includes both cancelled events, with zero values for all exhibition metrics, and completed events. The Total Index in Figure 3 and Figure 4 exclude cancelled events.

About CEIR

The Center for Exhibition Industry Research (CEIR) serves to advance the growth, awareness and value of exhibitions and other face-to-face marketing events by producing and delivering knowledge-based research tools that enable stakeholder organizations to enhance their ability to meet current and emerging customer needs, improve their business performance and strengthen their competitive position. For additional information, visit www.ceir.org.

###

Media Inquiries:

Mary Tucker

Sr. Communications & Content Manager

+1 (972) 687-9226

mtucker@ceir.org