Today, the Center for Exhibition Industry Research (CEIR) released the 2017 CEIR Index Report. The CEIR Index analyzes the 2016 exhibition industry and provides an economic and exhibition industry outlook for the next three years. Despite a decidedly mixed performance early in the year and worldwide political turmoil in the second half, U.S. economic growth proved resilient again in 2016, with GDP rising a moderate but unimpressive 1.6%. The economy once more was led by robust personal consumption expenditures as a result of expanding labor markets and recovering personal income. However, declining energy and equipment investment, a smaller inventory accumulation, and falling net exports partially offset relatively strong personal consumption expenditures to produce a seventh consecutive year of moderate growth.

Increasing employment combined with rising wages and low consumption price inflation spurred growth of real disposable personal income, which has been a bright spot in the U.S. economic record of the past several years. With robust job and personal income gains, a sharp recovery in energy-sector investment, an improving housing construction market, and rising nondefense capital goods orders, economic growth has momentum early in 2017.

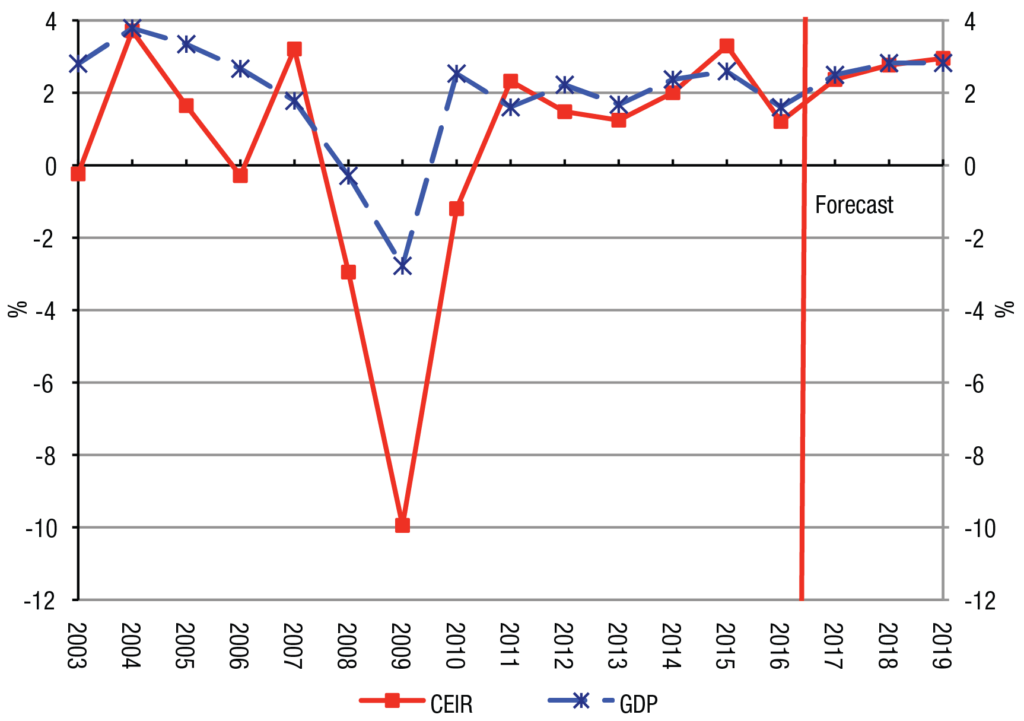

According to CEIR’s current projection, growth will pick up the pace to around 2.5% in 2017 before accelerating to 2.8% expansion in both 2018 and 2019 (see Figure 1).

Figure 1: Macro CEIR Index for the Overall Exhibition Industry, (2014=100)

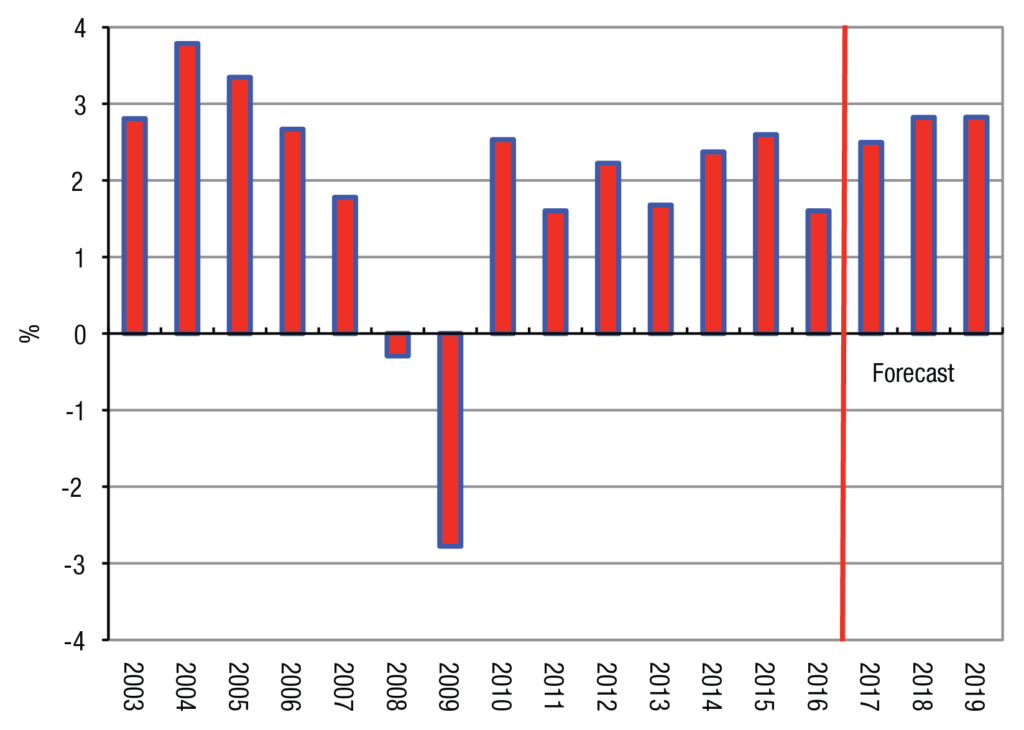

GDP growth in the next few years will be propelled by the consumer and private business sectors, as government expenditures will make only small contributions to growth in the foreseeable future. Net exports will continue to present a drag on the U.S. economy, as weak export and strong import demand leave a wide trade deficit (see Figure 2).

Figure 2: Annual Real GDP Growth

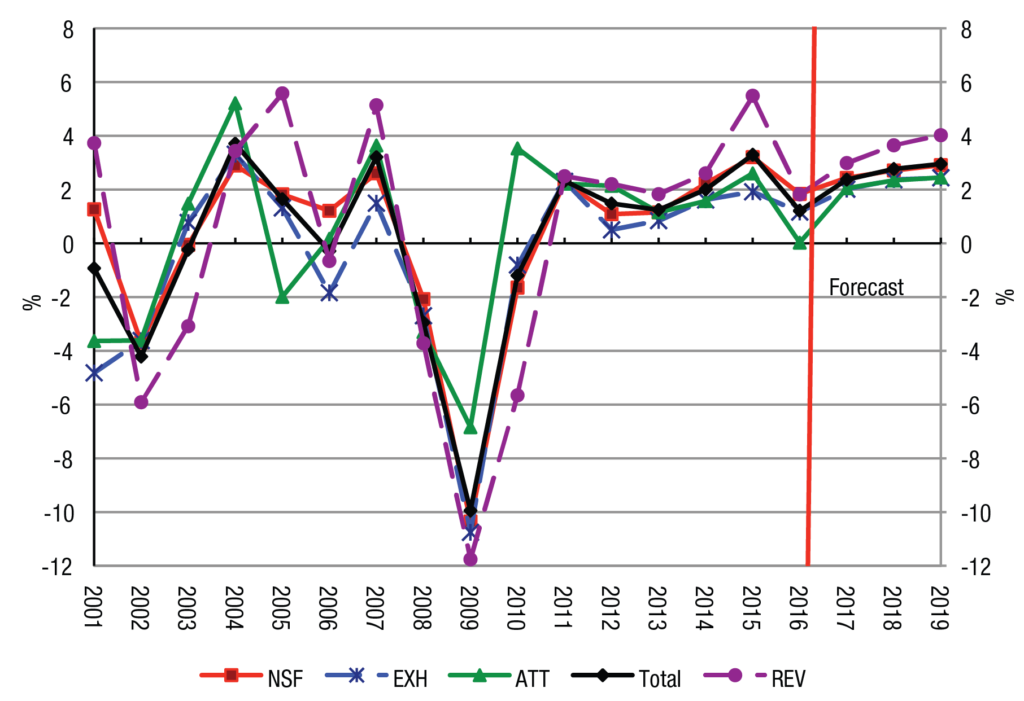

The performance of the business-to-business exhibition industry decelerated along with the macro economy in 2016. The CEIR Total Index, a measure of overall exhibition industry performance, increased by a modest 1.2%, 1.1 percentage points lower than in 2015. Nonetheless, three of four metrics rose in 2016: net square feet (NSF), real revenues, and exhibitors. Attendance levels were flat, which was primarily attributable to a substantial decline in Raw Materials and Science (RM) exhibition attendees (see Figure 3).

Figure 3: CEIR Index for the Overall Exhibition Industry, Percent Change

Exhibition developments in 2016 varied widely by industry. Leading sectors were Food (FD) and Building, Construction, Home and Repair (HM). On the other end of the spectrum, the weakest sector was RM, in which the index declined by 7.3%. This sector was plagued by low oil prices that led to declining investment and production levels, and subsequently RM exhibitions. The Industrial/Heavy Machinery and Finished Business Inputs (ID) sector registered the second largest decline of 4.5%, which in part was attributable to a correction after an impressive 11.0% jump in 2015.

“Economic and job growth should continue to drive expansion in all four exhibition metrics through the forecast period,” noted CEIR Economist Allen Shaw, Ph.D., Chief Economist for Global Economic Consulting Associates, Inc. “Despite a decline in 2016, ID and RM will grow more in line with their macroeconomic drivers. Their rebounds will help to push the overall CEIR Index growth to 2.4%, 1.2 percentage points higher than the 2016 rate but still 0.1 percentage point lower than real GDP growth. Exhibition performance will accelerate to 2.8% in 2018 and 3.0% in 2019 as the economy picks up its pace.”

The HM, ID, Communications and Information Technology (IT) and Transportation (TX) sectors will be driven by expansion of housing, auto sales and business fixed investment. Consumer-related exhibitions [Discretionary Consumer Goods and Services (CS); FD; and Sporting Goods, Travel and Amusement (ST)] will continue to benefit from strengthening household discretionary expenditures and are projected to increase by 2.8%. The outlook for Education (ED), Government (GV) and RM exhibitions remains somewhat pessimistic. The ED sector exhibited a secular decline over the last decade and a half, as tight government budgets restrained education and training spending. While some recovery from the decline should be visible in 2017, its growth will be limited. Government employment is likely to remain stagnant over the coming years, limiting potential attendance for exhibitions that cater to government services. Nonetheless, strong offerings in technology, safety and logistics will bring continued expansion of GV exhibitions.

As an objective measure of the annual performance of the exhibition industry, the CEIR Index measures year-over-year changes in four key metrics to determine overall performance: net square feet (NSF) of exhibit space sold; professional attendance; number of exhibiting companies; and gross revenue. The CEIR Index provides data on exhibition industry performance across 14 key industry sectors: Business Services (BZ); Consumer Goods and Services (CG); Discretionary Consumer Goods and Services (CS); Education (ED); Food (FD); Financial, Legal and Real Estate (FN); Government (GV); Building, Construction, Home and Repair (HM); Industrial/Heavy Machinery and Finished Business Inputs (ID); Communications and Information Technology (IT); Medical and Health Care (MD); Raw Materials and Science (RM); Sporting Goods, Travel and Entertainment (ST); and Transportation (TX). Click here for information on how to purchase the complete 2017 CEIR Index Report.

After its initial release, a forecast update of the CEIR Index will be presented at the CEIR Predict conference on 14-15 September 2017 at the Ritz-Carlton in Washington, D.C. For more information about CEIR Predict, visit www.ceir.org/predict.

“This will be our seventh annual Predict conference and we are eager to share new information and perspectives that industry executives have come to rely on from CEIR,” said CEIR CEO Cathy Breden, CAE, CMP. “The data from the latest CEIR Index, combined with the knowledge of guest economists, along with other forward looking sessions will provide attendees with an excellent predictive edge to use in their future strategic planning and business development efforts.”

CEIR sincerely appreciates the support it receives from this year’s Predict sponsors:

Title Sponsor

GES

Partner Sponsor

Freeman

Collaborator Sponsors

a2z, Inc.

McCormick Place/SMG

Synchronicities

Associate Sponsors

CNTV

CORT

Experient

Fern

New Orleans Convention & Visitors Bureau

Contributor Sponsors

4imprint

CMAC

Georgia World Congress Center

Hargrove

Oscar & Associates

For more information about the CEIR Index or CEIR Predict, contact Cathy Breden, CMP, CAE or call +1 (972) 687-9201.

About CEIR

The Center for Exhibition Industry Research (CEIR) serves to advance the growth, awareness and value of exhibitions and other face-to-face marketing events by producing and delivering research-based knowledge tools that enable stakeholder organizations to enhance their ability to meet current and emerging customer needs, improve their business performance and strengthen their competitive position. For additional information, visit www.ceir.org.

###

Media Inquiries:

Mary Tucker

Sr. PR/Communications Manager

+1 (972) 687-9226

mtucker@ceir.org